a) I am not as good at trading IV.

b) When you trade IV, you are essentially trading price so keep things simple and trade price.

Below is a more technical explanation of the above two statements.

Conversation on InformedTrades.com

I post a copy of this blog on InformedTrades. The following conversation took place between myself and another user (Forexer) on InformedTrades:

Forexer:

Here you about volatility. You think volatility follows the normal distribution? Price doesn't. Price is lognormal. They have skews very frequently and that is exactly what makes them tradable. I rather sell volatility than buy them because high IV usually erodes slowly at the least or maybe revert back to the mean. We can use statistics in trading volatility to a great extent. But we know its not all about volatility

Me:

Volatility is supposed to follow a normal distribution from what I understand. Reason being that the means of multiple lognormal distribution should be normally distributed. Since the means of the multiple lognormal distribution is basically what volatility is, we should conclude that volatility is normally distributed (correct me if I am wrong - been a while since I studied option theory).

But like price, I would argue volatility too should be lognormal because although volatility is supposed to measure the increase in price movement, [implied] volatility rises when price falls and vice versa. So IV really isn't measuring the variation in price but rather the market's belief or reaction to negative price movement. So, since price distribution can be skewed and volatility is simply the reaction to price movement, it too should be skewed.

Which brings me to my original point: if you trade IV's, you must take into account the fact that negative price movement will raise IV. So, you should long IV when you expect price to decline and vice versa. But why would you go into such complicated calculations when you could simply trade the price in the first place.

Hope all of that makes sense

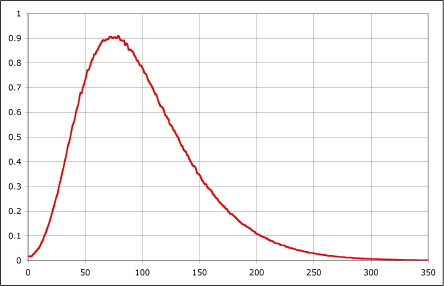

Let me explain that a little bit. A lognormal distribution looks like the graph below:

Source: danvk.org

Source: danvk.org The reason for this lognormal distribution is quite intuitive. The price can never fall below zero so the lower limit is set at zero. The upper limit is infinity however realistically speaking the price will be centered around the mean (which in this case is around 75).

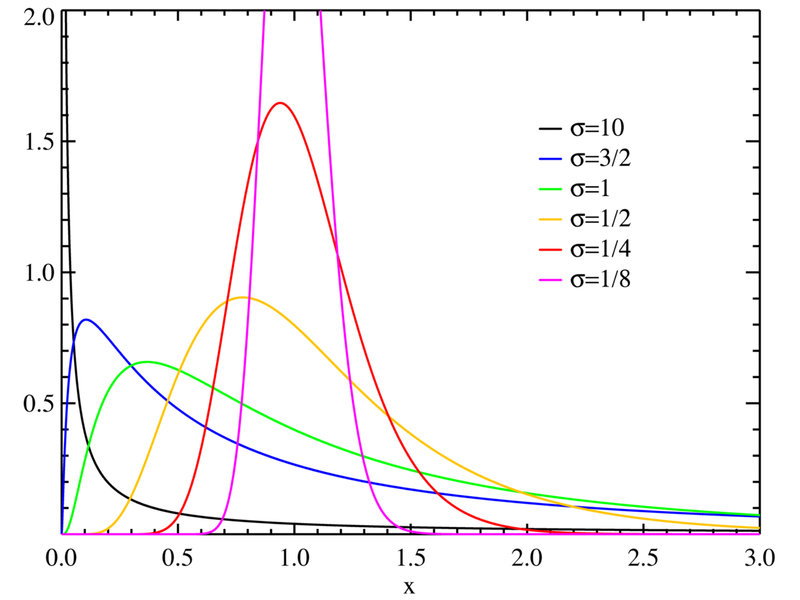

However, different set of price data for the same security can have a different lognormal distributions. The difference in this variation arises from variations in the mean and the standard deviations. For example (only illustrative), in the month of August, SPY could have a mean of 110 with a standard deviation of 10. In August, however, the average was 105 with a standard deviation of 20. These two data sets would yield two different lognormal shapes. This is illustrated in the graph below:

Theoretically, the means (averages) of all these lognormal distributions will have a normal distribution. In other words, if you created a data set of the means of all of the lognormal price distributions of a security and plotted it, the distribution would resemble the below:

Theoretically, this normal distribution is the volatility of the stock. But all of this seems counterintuitive to me. For one, remember that a normal distribution does not have a lower limit. So essentially you are allowing for negative prices - even if the chances are one in a billion. Additionally, and this is simply speaking for experience, IV tends to fall a lot slower than rise and this is clearly not represented in a normal distribution. Thus, there is a BIG disconnect in what IV actually is vs. what it theoretically is.

In my mind, IV is simply another way to say what the option's price is - which itself is simply a derivative of time value and underlying's price. Theoretically IV is supposed to imply how much the market believes the stock will move by expiration, but in truth, I believe it simply says "how afraid are people that stock will fall". The more afraid they are, the higher the IV (yes, even the call IVs - although this is often overlooked simply because the falling price deteriorates the price of calls).

Continuining with the coversation from above:

Forexer

Yea. Hats off to you. I'm not a math guy but i hear you on the IV being lognormal. Does IV increase on large updays?

Short answer: No. If anything IV falls on large updays. Take a look at the chart below of the SPY:

The chart shows SPY price plotted with average implied volatility. Granted this is not a very thorough study of IV vs. Price, but you can clearly see:

a) IV rises a lot quicker than it falls.

b) Price and IV are negatively correlated (When price rises, IV falls and vice versa). Notice the price vs. IV from Feb to May and then again from late June to August.

-Wown

stockjockz.blogspot.com

0 comments:

Post a Comment